|

| GTB Annual Report 2016 |

The primary set up is borrowing short term deposits from retail banking and lending short to medium term to the corporate sector. Around half the deposit base comes from the retail operation but this only accounts for 10% of the loans issued. This kind of business model is generally quite low risk and highly profitable.

The NIM is extremely high (9%+) in Nigeria but seems low outside Nigeria. This suggests GTB has a very good competitive position in Nigeria but that markets outside of Nigeria have relatively more difficult barriers to entry.

The high dividend yield of 8% is attractive by developed standards but is fairly priced given the risk presented by this kind of frontier investment. It is also subject to erosion via inflation and currency depreciation over time if the dividend growth cannot keep up with those forces.

Let us look at the some key risks;

Liquidity:

Loans are around 54% of assets and have dropped as a percentage of assets since 2015. Loans to deposits ratio is around 79% (2015;88.7%) so this has also fallen from 2015. This means that lending is able to be financed solely through the deposit base. Note also that cash has risen to 17% of assets (2015; 11%) showing a decent liquidity position.

The longer run liquidity of the bank looks reasonable. The deposit base is principally composed of short term deposits and accounts with very little long term deposits held (i.e time deposits). Therefore 82% of total funds are short term in duration at 0-3 months.

This is less precarious than it may sound though as lending is also generally short to medium term – although a liquidity gap does exist as 48% of total financial assets have a duration of 0-3 months. Generally the loan book shows durations as follow; 0-3 months – 36%, 3-12 months - 23%, 1-5 years – 36% and 5+ years 5%.

The key thing to remember though is that whilst the deposit base is not in time deposits of matching durations most of these balances are ‘sticky’ representing savings and current accounts of customers so the overall duration mismatch is not a significant structural problem.

It is also noteworthy that the longer run loans of one year or more are covered by the banks issued debt securities. These longer run balances are mostly USD as Naira is too inflationary for long term lending. Therefore the bank only requires capital markets for long run lending and can fund its short duration loans and overdrafts from its deposit base.

I think the liquidity risk to Guaranty is thus low.

Credit risk:

Capital adequacy is very respectable at 20% with a low 5x leverage ratio.

The majority (>80%) of other securities (restricted deposits and investment securities) forming the bulk of the other financial assets of the bank are held in Nigerian central bank securities and deposits.

In terms of international risk around 90% of loans are concentrated in Nigeria. The bank has overseas subsidiaries in other areas of Africa where the residual 10% of loans are situation. So the loan base in general is principally a play on domestic Nigerian factors rather than pan regional growth.

More of a concern is that the bank’s corporate loan book exposure to Oil & Gas is around 40%. Given the depressed state of the industry in Nigeria this is a risk to the bank’s loans. The next most significant sector is Manufacturing with 18% of loans being extended here.

Note that Nigeria is in recession so we should expect asset quality generally to be poor from a cyclical perspective at this time.

Asset quality is not great by developed standards with loan allowances running around 5% of loans. However this has been stable over the past two years and appears to be more a structural hazard to lending than a significant downtrend. NPLs have trended up slightly over the period to 3.66% from 3.21% but again this is actually lower than historically stronger macro years such as 2012 when it was 3.75%.

Asset quality seems reasonable given the recessionary context and frontier market macro.

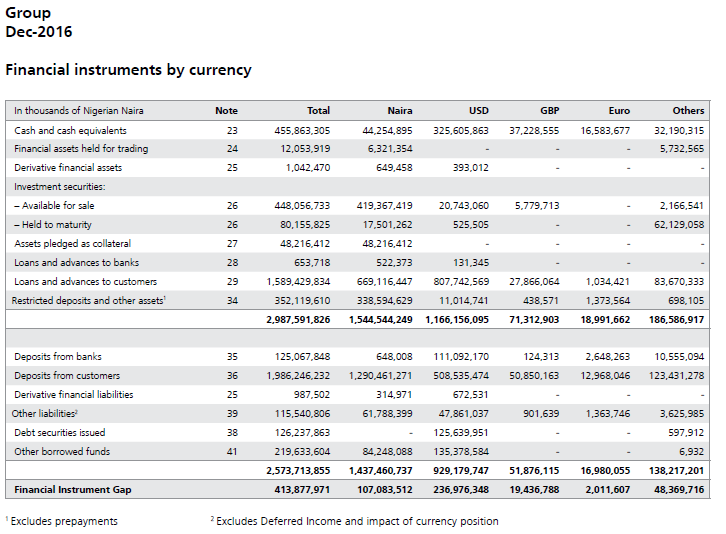

Currency Risk:

The risk is the mismatch in USD lending with deposits. The bank has a reasonable sized funding gap in USD which is a risk should a substantial further deterioration in the currency occur. The bank has 50% of loans extended in USD and further 71% of all cash is held in USD. The bank however has only 25% of deposits in USD and then its USD issued debt securities.

|

| GTB Annual Report 2016 |

The upshot of this is that the bank is overextended in dollar loans compared to its deposit base but it makes up for this in wholesale funding. In a sense this works well in an economy where you expect your currency to depreciate as a weaker Naira means in local currency terms that your asset base grows faster than you deposit base.

Note they do have dollars to hand – in fact they have surplus cash in dollars meaning a lot of liquidity still available to lend. The risk to the bank is a run on dollar deposits meaning they have to try to secure additional dollars at unfavourable rates or capped volumes due to continued currency controls.

Generally however the dollar side of the balance sheet means a portion of the value of the bank should be retained or even enhanced by further devaluation.

Currency risk is high but the bank is positioned well to counter this.

Earnings:

The bank has had substantial gain in 'Other Income' from the Naira devaluation due to the composition of the balance sheet. This has rather flattered earnings in 2016 with the PE rising from 6x to ~30x without this - it is highly likely that some of this is non recurring but the gain does offset the effects of the slowdown in Nigeria from the recession.

Normalizing these gains I expect during 2017 the bank will trade around 10-12x earnings which is fairly valued for a bank.

Summary:

The way I see it ultimately GTB is a play on Nigeria macro and in turn that relies on higher oil prices. I see short to medium term pressure on oil prices continuing but given the devaluation that has occurred in combination with a slight pick up in reserves I feel the worst may be priced in for Nigeria at this point.

|

| GTB Annual Report 2016; Limited profitability outside Nigera |

Much of my case to own GTB is that it acts like an option. Within its context this is a relatively low risk bank and one of the more established players in Nigeria. This means it is unlikely to go bust in my opinion in the medium term as it has few real structural issues.

Much like Argentine banks in the Kirschner period I feel that GTB can grow quite happily inline with inflation – likely returning little to investors while the currency depreciates – but one is biding time here waiting for the next oil upcycle. Nigerian domestic opportunity is huge but so is the risk.

Still I feel on balance that taking a small position in GTB is appropriate and I have done so already. Sometimes I find it beneficial to take a starter position and get more interested in the stock from there. There is still a lot to consider but the investment case is a little more top down than I usually like to do but it is because the bottom up is so driven by macro rather than simple structural trends.

Disclaimer: I have an interest in Guaranty Trust Bank (LON:GRTB) at present. These are opinions only, not investment advice. If in doubt read my disclaimer.

No comments:

Post a Comment